|

With 2020 behind us, many businesses are now in recovery mode. This year will be one of budget repair for most businesses through developing long term strategies. Here are some issues all small to medium businesses should consider to ensure their survival.

1. Build client or customer relationships A priority as once COVID-19 hit how many businesses have had the time to do this proactively? Cost-cutting, streamlining operations, implementing new health and safety procedures were the focus. It is now time to revisit customer relationships and how to support them for mutual benefit. If your customer base has changed, focus on building new relationships to deliver repeat business in the future. Ask yourself what the real value of each customer and the cost to you is to get them. New customers generally cost more to acquire than maintaining existing ones. However, this is sometimes not the case. You may spend more time and money serving low-value clients, and those precious resources would be better spent forming new relationships. We have seen a significant number of family-run businesses breakdown due to financial distress in the last twelve months. By the time a business is in financial distress, strained family relationships are often compounded further with money worries. If you're setting out to establish a business with family members, it is vital to recognise the inherent risks.

Our advisory team assists many people and companies in financial distress. Our unique expertise allows us to provide solutions across a wide range of financial distress issues that companies and individuals experience.

We negotiate daily with debt collection agencies and importantly understand both debtor and creditor's rights and obligations. Debt collection agencies should be flexible in their approach. A flexible approach involves making meaningful and sustainable payment arrangements that reasonably consider a debtor's ongoing living expenses. The ACCC and ASIC have produced a debt collection guideline for debtors and creditors, which encourages flexibility on the part of both parties. The guide includes recognising debtors who are vulnerable and experiencing financial hardship and appreciating that debtors may have several debts owing to different parties. If you have to deal with a debt collection agency on your own, be sure to reference this guide. Another helpful resource to access if you are comfortable dealing with a debt collection agency on your own is visiting the AFCA Datacube. The AFCA Datacube shows you the number of complaints against a debt collection company over the last twelve months. If you have any questions or need assistance, our team offer a cost-free consultation and can be contacted on 02 8304 9300. Susie Barnett established SR Group over a decade ago in Australia. With the success of our business in Australia, we are thrilled to be expanding our team in New Zealand. We are a dedicated team that helps people confronted with financial distress and victims of financial impropriety.

Read more http://www.gisborneherald.co.nz/business/20200907/advocate-for-victims-of-fraud-financial-distress/  In Australia, financial counselling is a free and confidential service provided by community organisations, community legal aid and some government agencies. It is an essential service for over 125,000 people each year experiencing financial distress. Financial counsellors are skilled in listening to problems when an individual's judgement and clarity may be distorted. What people need is non-judgemental and confidential advice plus a workable plan to improve their financial distress situation.

The effects of COVID-19 have been devastating for businesses across the country, but for many, there is a silver lining. Companies have adapted and transitioned employees to work remotely with great success. COVID‑19 will be with us for some time, so it is essential that your business has a plan - and continues to plan to keep your workplace healthy, safe and virus-free. Key things to remember as you ramp up your business post COVID-19.

Keeping People Safe Maintain good hygiene - Think about how your business’s hygiene and cleaning practices by making sure your workplace is regularly cleaned and disinfected. Have enough cleaning and hygiene supplies and communicate the importance of employees not coming to work if they are unwell. Stay physically distant - Think about how people interact in your business. To ensure your business has appropriate physical distancing move work stations and tables further apart to comply with social distancing. If you are a retailer, provide social distancing markers on the floor where appropriate. In the event of infection, there should be a plan in place, so your business is confident and can respond swiftly and efficiently. Follow advice - Think about what makes your business and your industry unique. There may be additional steps you need to take to communicate with your customers, staff and suppliers. To help you prepare regularly review the mandatory public health directions that apply to your business as these will change as time goes on. Sustainability is important – many of these changes, such as cleaning practices, will be part of your day-to-day business operations already. Still, you may need to do things more often or in different ways. A helpful resource is safeworkaustralia.gov.au Adapting my business The way your business operates, the products you sell and the services you deliver may need to change because of COVID‑19. This transition will be challenging, and you are no doubt thinking about how your business could adapt to change. It is helpful to spend some time thinking about the following questions. These can act as a starting point to map potential areas for your business to explore.

Accessing Support and Packages When considering adapting your business activities and your employees you may need financial support to achieve your new plans. The Federal, State, Territory and Local Government are providing many support packages for businesses. These are the current support packages you can apply for: Retaining your employees

Small and medium-sized businesses can get loans of up to $250,000 over three years from a range of lenders. These loans have an initial six month repayment holiday. Enquire with your lender. Over the coming months, many businesses will rely on these packages to kickstart and adapt their business activities. Our advisory team has been supporting many of our clients in these challenging times. If you need any assistance with financial support packages and solutions, we are here to assist. Our services range from general hardship relief, loans and mortgage moratorium, vehicle and equipment finance, ATO issues and leasing arrangements. Please phone us on +61 2 8304 9302 to speak to a dedicated team member. Being in personal or credit card debt can unravel a myriad of lies you tell yourself, hoping the money problems will disappear. Still, if not appropriately managed, it can leave you in financial distress.

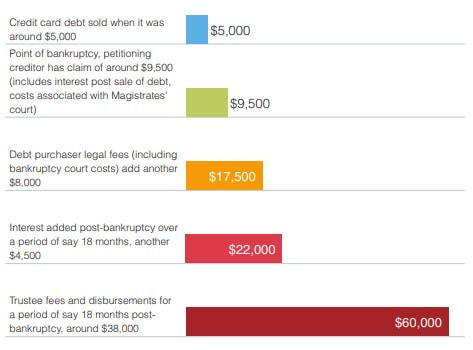

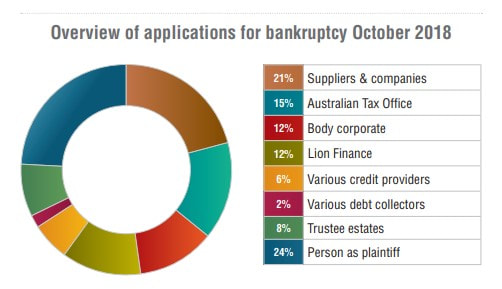

There are standard lies we tell ourselves about debt. If you relate to these, it is time to acknowledge it, so that you can change them before they become problems. At the SR Group, we understand the experience of being forced into bankruptcy is highly stressful for people. It involves court proceedings, substantial costs, the need for legal advice and very often the fear of losing the family home. A person can be bankrupted on a debt as little as $5,000. This amount can balloon to many thousands after legal costs and fees are added. The following example is from the casework of Consumer Action Law Centre and involved a client who had an initial credit card debt of around $5,000. The amount outstanding 18 months after the forced bankruptcy was around $60,000. This how the debt can accumulate:  Source: Consumer Action Law Centre July 2019 Article: ‘Who is making Australians bankrupt?’ This can mean that a small credit card debt could lead to the loss of the family home. Many people being made bankrupt are in financial hardship and could make a repayment arrangement to pay their debts if given the opportunity. Forced bankruptcy should be a last resort. SR Group seeks to avoid this burden for our clients. Constructively working with people in financial hardship gives them an opportunity to repay their debts. Extra time can mean the person is able to improve their financial position, for example, to recover from an illness or get back to work. In October 2018 alone, there were 265 filings for bankruptcy in total. The biggest percentage of filings involved individuals and various companies suing over debts. The next largest percentage of filings is the Australian Taxation Office (15%), followed by publicly listed debt collector, Lion Finance (12%), and then various corporate bodies (strata plans/owners corporations) (12%).  Source: Consumer Action Law Centre July 2019 Article: ‘Who is making Australians bankrupt?’ SR Group achieves success with creditors through lump-sum settlements, mediation and negotiation. Credit Negotiation Case StudyBACKGROUND We provided advisory services to the director of a company that provided financial solutions to businesses who sold small ticket items. Our client’s company had operated successfully for several years before a combination of environmental and market conditions caused a significant downturn in revenue. After numerous attempts to revitalise the business and diversify, and in keeping with his directorship duties, our client made the decision to wind up his company and appoint a liquidator. After appointing the liquidator, our client found employment in a managerial role in a different company. While, the salary of the new role covered his living expenses, it did not leave enough money for him to meet his monthly creditor repayments, which were in substantial arrears. However, our client did not want to abrogate his personal creditor responsibilities and take the personal insolvency route. ACTIONS TAKEN TO ASSIST & OUR RESULT We acted on behalf of our client in aiming to settle each of his eight debt collectors (St. George, ANZ, Visa, NAB, Westpac, Prospa, Baycorp, Citibank) for the lowest possible amount on the grounds of financial hardship. A family member of our client generously offered a small pool of funds to help settle his creditors. Overall, we were able to reduce our client’s debt from $261,000 to $84,000, a reduction of 68%. Our client now only had to pay 32 cents in the dollar, which he had to do immediately upon receipt of each offer in the form of a discount lump-sum settlement. ATOThe most prolific user of the bankruptcy system is the Australian Taxation Office (ATO), which applied to make 543 people bankrupt in the past financial year of 2018-19. This number, however, was significantly lower than in the past three financial years. In the 2015-16 financial year the ATO applied to the Federal Court to make 1,215 people bankrupt. This fell to 1,061 people in 2016-17. In 2017-18 that number had fallen further to 833. SR Group helps assist clients with ATO issues through seeking:

The Commissioner of Taxation can release a person from a tax debt if making the payment would cause serious hardship. Serious hardship is defined as where the payment of a tax liability would result in a person being left without the means to afford basics such as food, clothing, medical supplies, accommodation or education. If the serious hardship standard is met (as determined by the ATO), then the person may be able to be released from all or part of the tax debt. Through our experience it must be noted that serious financial hardship can be a difficult standard to meet. SR Group has a proven track record in negotiating with the ATO to reach a mutually agreeable resolve. ATO Case StudyBACKGROUND

An established travel agency established in 1998 incurred financial distress, due to ongoing family health issues over a 10-month period. This difficult period resulted in neglect of the business, which ultimately led to a winding up application from the Australian Taxation Office (ATO). ACTIONS TAKEN TO ASSIST & OUR RESULT On behalf of our client, we negotiated with the ATO through various correspondences and reached a settlement equivalent to 48% of the initial debt. We achieved a full remission of interest and penalties on the debt, as well as establishing a monthly payment plan over two years to settle the debt, allowing the client to effectively manage their cash flow as the business got back on its feet. DIRECTOR'S TESTIMONIAL “I recently used the services of the SR Group and cannot recommend them highly enough. In particular I dealt with the Client Relations Manager Mandana Missaghi, her professionalism, diligence and empathy helped me through a particularly difficult situation. Mandana has a very understanding and positive attitude which I really appreciated through all our dealings. The SR Group thoroughly investigated my situation, guided me through the available options & then negotiated on my behalf to reach an agreeable solution. I cannot thank the SR Group enough for their assistance & advice.”  Between managing company finances, meeting taxation requirements and keeping your staff paid, as well as running a profitable and competitive business, managing a small business can certainly be a big job. It’s easy to get caught up in the day-to-day operations of the business and neglect your overarching responsibilities, but we must ensure we don’t fall into this trap, as this often leads to a downward spiral which can be impossible to recover from. Managing your cash flow properly will go a long way to helping you stay on top of the ongoing taxation and employee obligations in your capacity as director. As an accountant, you should be communicating regularly and clearly with your clients to ensure they fully understand their cash flow position and cash forecast for the next few months.

Mali De Castro  As 2017 starts to wind down, we begin to cast our eye forward towards the year to come. Here at the SR Group, we work closely with many small business owners and company directors, and we have decided to compile a list of tips to help your business thrive in 2018. |