|

With 2020 behind us, many businesses are now in recovery mode. This year will be one of budget repair for most businesses through developing long term strategies. Here are some issues all small to medium businesses should consider to ensure their survival.

1. Build client or customer relationships A priority as once COVID-19 hit how many businesses have had the time to do this proactively? Cost-cutting, streamlining operations, implementing new health and safety procedures were the focus. It is now time to revisit customer relationships and how to support them for mutual benefit. If your customer base has changed, focus on building new relationships to deliver repeat business in the future. Ask yourself what the real value of each customer and the cost to you is to get them. New customers generally cost more to acquire than maintaining existing ones. However, this is sometimes not the case. You may spend more time and money serving low-value clients, and those precious resources would be better spent forming new relationships. For many victims of financial disputes, it can be a daunting process to navigate recovering your funds. You may have tried to resolve the issue with the financial provider and have had no response or success.

Where do you go next? The Australian Financial Complaints Authority (AFCA) is a non-government dispute resolution organisation providing free, fair and independent help with disputes between consumers and financial providers. It is compulsory for all Australian Financial Services Licence and Australian Credit Licence providers to be members of AFCA. To have a complaint considered by AFCA it has to be within six years after you first became aware of the loss. With an exception of the current one-year window to consider complaints dating back to 1 January 2008. AFCA is only allowed to accept legacy complaints until 30 June 2020. 2019-20 Federal Budget

Last week saw the first Federal Budget in the wake of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry. The Federal Government announced they will provide $606.7 million over five years in response to the Royal Commission: Use of Funding Amount $2.6 million - Designing and implementing an industry-funded compensation scheme of last resort (CSLR) for consumers and small businesses. $2.8 million - Providing the Australian Financial Complaints Authority (AFCA) with additional funding to help establish a historical redress scheme to consider eligible financial complaints dating back to 1 January 2008. $30.7 million - Paying compensation owed to consumers and small businesses from legacy unpaid external dispute resolution determinations. $404.8 million - Resourcing the Australian Securities and Investments Commission (ASIC) to implement it new enforcement strategy and expand its capabilities and roles in accordance with the recommendations of the Royal Commission. $145.0 million - Resourcing the Australian Prudential Regulation Authority (APRA) to strengthen its supervisory and enforcement activities which will support its response to key areas of concern raised by the Royal Commission, including with respect to governance, culture and remuneration. $7.7 million - Establishing an independent financial regulator oversight authority, to assess and report on the effectiveness of ASIC and APRA in discharging their functions and meeting their statutory objectives. $1.0 million - Undertaking a capability review of APRA, which will examine its effectiveness and efficiency in delivering its statutory mandate, as well as its capability to respond to the Royal Commission. $11.2 million - Establishing a Financial Services Reform Implementation Taskforce within the Treasury to implement the government’s response to the Royal Commission, and co-ordinate reform efforts with APRA, ASIC and other agencies through an implementation steering committee. $0.9 million - Providing the Office of Parliamentary Counsel with additional funding for the volume of the legislative drafting that will be required to implement the government’s response to the Royal Commission. ASIC has largely won a landmark case against Melbourne businessman Bill Lewski, former federal health minister Michael Wooldridge and other directors of failed property group Prime Trust, with the High Court ruling the men had breached their duties as directors. The High Court found it “cannot ignore the injustice caused to members by an amendment that permits $33 million of their equity to be paid away without authority”. The Federal Court is to reassess the penalties and disqualification periods for the directors.

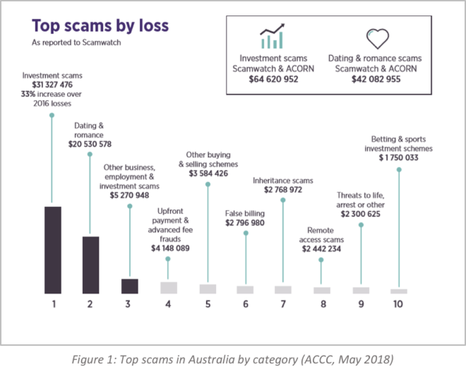

In 2017, Australian’s lost A$31.3 million to investment fraud schemes, per the May 2018 report by the Australian Competition and Consumer Commission (ACCC). This figure is almost certainly an under-representation on the total amount lost, as investment fraud is one of Australia’s least reported crimes, mostly due to shame or embarrassment of the victims. But don’t be embarrassed, investment frauds are becoming more sophisticated and harder to recognise, and with over 200,000 reports of scams last year, you are certainly not alone.  Next step: award compensation to the investors she defrauded!A WA businesswoman under investigation for masterminding a suspected $180 million “Ponzi” scheme, in which Malaysian and Singaporean investors were courted to invest in Pilbara property, has been permanently banned from providing financial services.

Australia’s corporate watchdog, the Australian Securities and Investments Commission (ASIC), has found Veronica Macpherson engaged in “misleading” and “deceptive” conduct while promoting the Newman Estate Project in Western Australia’s Pilbara to overseas investors. |